When you go to book a flight, it’s not uncommon to be prompted to purchase trip insurance on top of your fare. If you decline the option, you might get a warning: “You may be responsible for cancellation fees and delay expenses” or, if that doesn’t scare you enough, “The average out-of-pocket costs of medical emergency transportation outside the United States can be as high as $25,000.” Those are potentially frightful consequences, but you should think twice before handing over the extra money. It’s probably not in your best interest as a higher flyer, and believe it or not, getting it might cost you more than it’s worth.

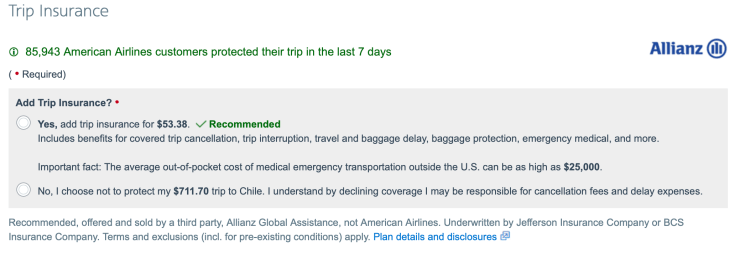

As more and more people have been taking to the skies, whole businesses and services have popped up to support (or if you’re cynical, take advantage of) these new travelers. There’s a whole host of paid online courses to help nervous flyers quell their fears, for example; in a similar vein, various insurance providers have introduced policies designed to help travelers protect their investments. The latter has become so commonplace that, right before you hit “Book” on American Airlines’s website — every single time you want to buy a fare — you’ll see something to the extent of “Would you like to add trip insurance?”

In fact, you can’t even click the button to purchase your ticket until you’ve chosen either “Yes” or “No” on insurance. That’s frustrating and manipulative, but AA is hardly alone. Delta makes its customers do the same…

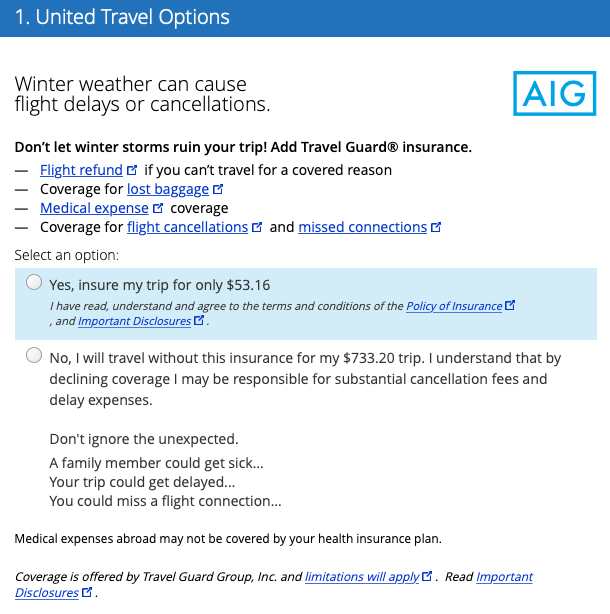

And so does United, which takes the sales pitch one step further by adding a list of hypothetical worst-case scenarios right underneath the “No” option. “Not willing to pay for insurance?” United and its partner, AIG, seem to ask, “But what if your family member DIES?!?”

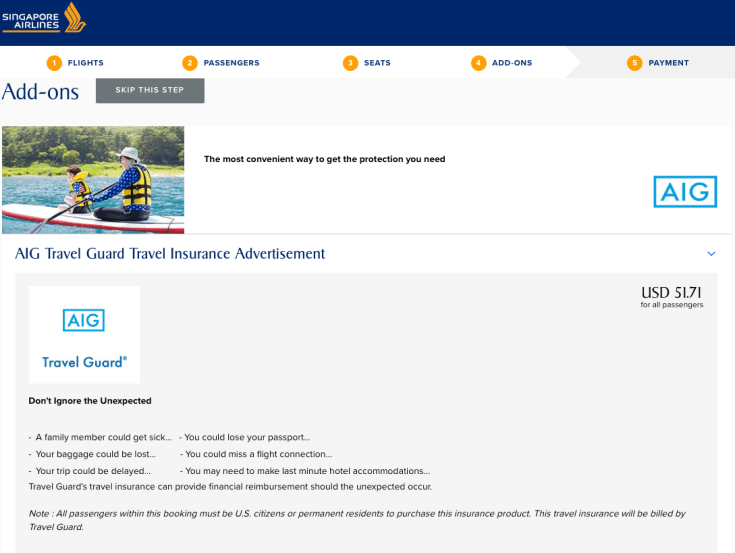

Foreign carriers participate in this trend/blatant act of opportunism too. United’s Star Alliance partner Singapore Airlines is hardly alone in making its passengers choose whether or not they want to “ignore the unexpected,” but at least it’s candid and correctly identifies this prompt as an advertisement.

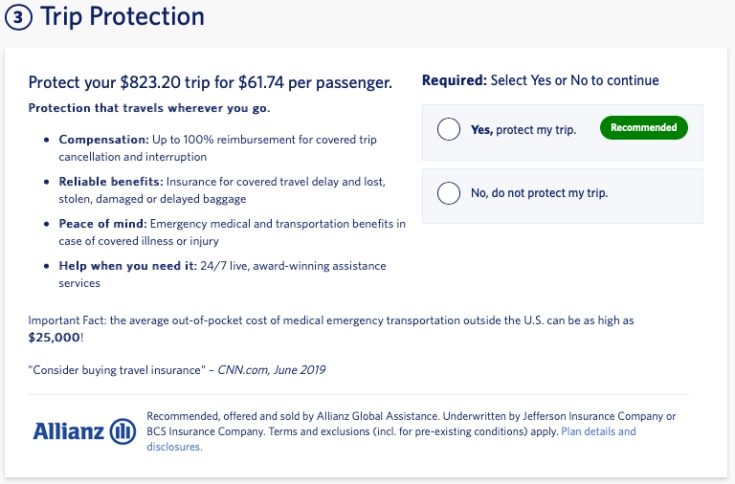

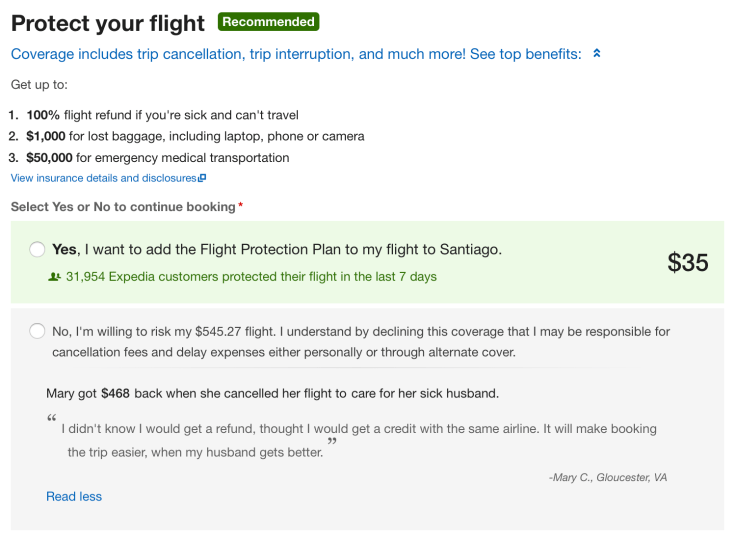

And of course, online travel agencies do this too. They are, in fact, the ones that pioneered this “added feature.” The example pictured below is from Expedia, but note that pretty much every single OTA does this. You’ll see this or something like this everywhere on the internet where you might book a flight.

There’s a simple reason why you see pitches for trip insurance so frequently: these policies are so, so lucrative and the companies providing them are so, so effective at marketing them. There’s nothing wrong for this practice per se — clearly people are willing to pay for the peace of mind that insurance provides — but the demand for it seems to be artificially bolstered. The fact that choosing “yes” or “no” is mandatory is irritating, sure, but the use of fear tactics is outright manipulative.

Notice how pretty much every ad (except Singapore’s) reminds you, the customer, how much you spent on a ticket. A lot of the “No” options read: “I choose not to protect my $$$ trip.” Potentially, that figure is a huge some of money AND, for a marginal amount more, you wouldn’t have to worry at all. If that’s not enough to compel you, you’ll read about all the things you’d be protected from because of this insurance. Don’t want to risk getting caught in a blizzard? Buy the insurance!

But here’s the thing: these policies likely cost a lot more than they’re worth and they seldom represent a good value for your money. I won’t go far to say that trip insurance is a scam, but there are two things you ought to be aware of before clicking “Yes, protect my trip!”

1. There’s a good chance you already have trip insurance

If you have a travel credit card that you pay an annual fee for, you’re almost certainly already covered by trip insurance. Every major flexible currency credit card, as well as every noteworthy cobranded card, offers trip insurance as a benefit. Don’t believe me? Well, all of the following include it…

- American Express Platinum and Gold cards

- Capital One Venture and Spark cards

- Chase Sapphire Reserve, Preferred, and Ink cards

- Citi Prestige and Premier cards

- All American Airlines credit cards

- All Delta cobranded credit cards

- All Southwest cobranded credit cards

- All United cobranded credit cards

- All Hilton cobranded credit cards

- All Hyatt cobranded credit cards

- All IHG cobranded credit cards

- All Marriott cobranded credit cards

…Among many, many others. Hell, even Spirit’s and Frontier’s cards offer trip insurance!

So, if you’re using any one of those cards to pay for your trip, you’ll already have trip insurance. Why bother paying twice (ie once with the annual fee and once again when you choose “Yes”) for something? There is no value-added when you buy from the airline/the OTA either; the coverage will be near identical.

2. Trip insurance is not the same as a refundable ticket

There’s a common misconception about trip insurance, and it’s that if anything goes wrong, you’ll be reimbursed. That, however, is only technically true; there has to be a genuine logistical catastrophe if you want to have any hope of seeing some cash back. This is confirmed in the “fine print” of each policy, and despite there being multiple different companies with their own offerings, they’re all pretty much the same in practice. They all require you to jump through hoops to actually see the benefits of the coverage you paid for.

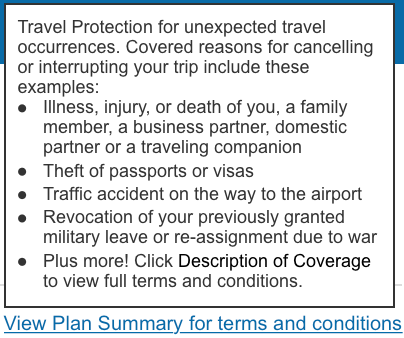

Moreover, there are four main conditions in which you can get (some of) your money back. They are if you and/or someone in your traveling party…

- Gets sick and/or dies.

- Has a passport/visa stolen.

- Gets in to a car accident en route to the airport.

- Is compelled in to active duty military service.

And that’s about it. There are some exceptions from policy to policy, but those are the highlights. As for other things that could go wrong, well, there are so, so many restrictions in place that might prevent you from being reimbursed. Look at this actual policy offered by Allianz if you need further convincing. Here’s another from AIG. Good luck trying to make sense of it all.

But seriously, what if you…

- Are urgently summoned for a shift at your job?

- Get a cold, cancel your trip, but don’t go to the doctor?

- Suffer a series of financial setbacks and can’t afford to go?

- Decide that you don’t want to go any more? (For example: would you want to go to Chile or Hong Kong right now given the recent outbreaks of political unrest?)

…then you’d be on the hook for those expenses EVEN IF you signed up for insurance. What’s the point of paying extra if it can’t help you in those far too common unfortunate events?

You’d hope that trip insurance would provide broader coverage than for just a few rare, unlikely and unlucky situations, but alas. That wouldn’t be as profitable for the companies (but that’s a different rant for a different blog), and besides, you could just buy a refundable-yet-significantly-more-expensive ticket to get the more comprehensive protections you might need instead.

…But then again…

Trip insurance could make sense for you. For one, if you don’t already get it through your credit card (like what if you pay for your airfare with a debit card?) then it might be a good value, but only if you don’t already have it! Otherwise you’re just wasting your money.

But say you don’t already have it AND you’re old or have young children or suffer from health problems or all of the above. Then trip insurance could actually make a lot of sense. What if grandpa gets sick and can’t fly with the rest of the family? Or worse, what if he gets really sick away from home? In either case, you would be able to recoup most, if not all, of your expenses paid.

Then again of course, the fear of “what if” is how the insurance companies are able to market their products. Is the peace of mind worth the hassle of spending more money? Only you can answer that.

1 Pingback